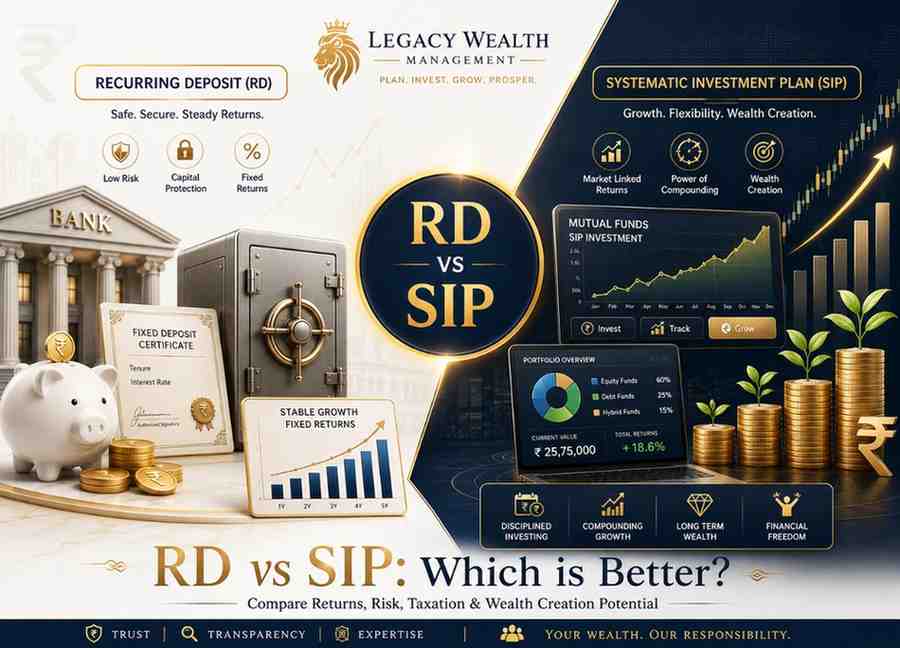

RD vs SIP: Which one is Better

June 20th, 2026 News

RD vs SIP: Which is the Better Investment Option in 2026?

If you're looking to build wealth steadily, you've probably come across two popular options: Recurring Deposit (RD) and Systematic Investment Plan (SIP). Both let you invest small amounts regularly, but they work very differently and can lead to very different outcomes.

In this guide, we'll compare RD vs SIP on returns, risk, taxation, and liquidity — so you can make an informed choice. For personalized guidance, Wealthifyme, the best mutual fund distributor in Faridabad, can help you pick a plan suited to your goals.

What is RD (Recurring Deposit)?

A Recurring Deposit is a traditional savings instrument offered by banks and post offices. You deposit a fixed amount every month, and at maturity, you receive the principal plus interest.

Features of RD

- Fixed returns: Interest rate (typically 5–7%) is locked in and doesn't change with the market. (Compare with NBFC Fixed Deposits for similarly stable, higher-interest options.)

- Low risk: Backed by banks, making it very safe.

- Guaranteed maturity amount: You know exactly what you'll get.

- Penalty on premature withdrawal: Breaking an RD early reduces your returns.

What is SIP (Systematic Investment Plan)?

A SIP is a method of investing in mutual funds where a fixed amount is invested at regular intervals instead of a lump sum.

Features of SIP

- Market-linked returns: Depends on the performance of the chosen fund (equity, debt, or hybrid).

- Power of compounding: Long-term SIPs benefit significantly from compound growth.

- Rupee cost averaging: Reduces the impact of market volatility over time.

- Flexibility: Increase, decrease, pause, or stop anytime.

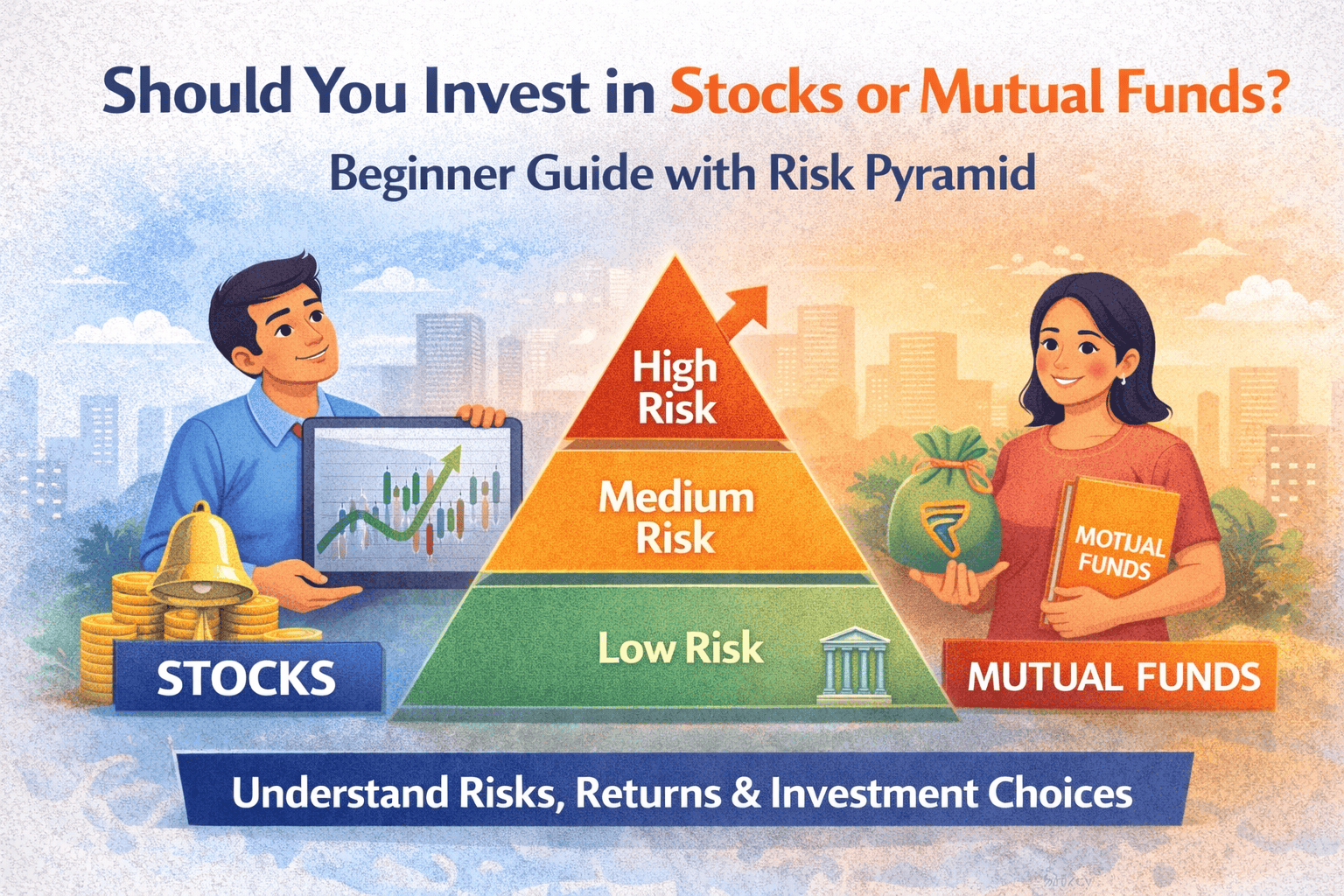

RD vs SIP: Key Differences

| Parameter | RD | SIP |

|---|---|---|

| Returns | Fixed (5–7%) | Market-linked (historically 10–15% in equity funds) |

| Risk | Very low | Low to high, depending on fund type |

| Liquidity | Moderate, penalty on early exit | High, easy redemption |

| Taxation | Interest fully taxable | Depends on fund type & holding period |

| Best For | Short-term, risk-averse goals |

Long-term wealth creation |

RD vs SIP: Returns Comparison

For a monthly investment of ₹5,000 over 10 years:

- An RD at 6.5% interest accumulates roughly ₹8.5–8.7 lakh.

- An equity SIP averaging 12% could accumulate ₹11.5 lakh or more.

The gap widens further over 15–20 years due to compounding, making SIP a stronger option for long-term wealth creation (though past performance never guarantees future results). Use our free SIP calculator to estimate your own returns based on your monthly investment and tenure.

Risk and Taxation

- RD carries minimal risk — it's bank-backed and insured up to ₹5 lakh under DICGC. RD interest is fully taxable as per your income slab.

- SIP carries market risk, which smoothens out over longer horizons. For equity funds, long-term gains above ₹1.25 lakh are taxed at 12.5%; short-term gains at 20%. Debt fund SIPs are taxed as per your income slab.

SIPs, especially long-term equity ones, are often more tax-efficient than RD interest.

Which One Should You Choose?

Choose RD if:

- You want guaranteed, fixed returns.

- Your goal is short-term (1–3 years).

- You have zero tolerance for market risk.

Choose SIP if:

- You're investing for long-term goals like retirement or a child's education.

- You can tolerate moderate market fluctuations.

- You want better inflation-adjusted returns.

For most investors with a 5+ year horizon, SIP tends to outperform RD — but choosing the right fund matters just as much as choosing SIP over RD. Our goal-based investing approach helps you map the right SIP to each specific life goal.

Why Consult Wealthifyme — The Best Mutual Fund Distributor in Faridabad?

Picking between RD and SIP — and selecting the right fund — depends on your income, goals, and risk tolerance. Wealthifyme, the best mutual fund distributor in Faridabad, can help you:

- Assess your goals and risk appetite accurately

- Recommend SIP plans suited to your time horizon

- Diversify across equity, debt, and hybrid funds

- Review and rebalance your portfolio periodically

Whether you're a first-time investor or optimizing an existing portfolio, expert guidance from Wealthifyme ensures your money works harder for you, with plans tailored specifically to your financial journey.

How to Start a SIP with Wealthifyme

- Define your goal – retirement, child's education, home purchase, or wealth creation.

- Assess your risk profile – conservative, moderate, or aggressive.

- Get a free consultation from Wealthifyme, a trusted mutual fund distributor in Faridabad.

- Select the right SIP plan based on fund performance, expense ratio, and fund manager track record.

- Start small and stay consistent – even ₹1,000–₹5,000 a month can grow significantly over time.

- Review periodically with the Wealthifyme team to stay aligned with your goals.

Liquidity: A Quick Note

One more factor worth considering is liquidity. RDs come with a lock-in style structure — you can withdraw early, but you'll usually lose part of the interest as a penalty. SIPs in open-ended mutual funds, on the other hand, offer much higher liquidity, with most redemptions processed within 1–3 business days. The only exception is ELSS funds, which have a mandatory 3-year lock-in. If easy access to your money matters to you, this is an important point to weigh alongside returns and risk.

Conclusion

RD offers safety and predictability, ideal for short-term, low-risk needs. SIP offers the potential for higher, inflation-beating returns through disciplined long-term investing. If you're unsure which option fits your goals, speak to Wealthifyme — the best mutual fund distributor in Faridabad — for personalized, goal-based advice.

Ready to start your investment journey? Connect with Wealthifyme today for a free, no-obligation portfolio consultation and find the right RD or SIP strategy for your financial goals.

FAQs

1. Is SIP better than RD for long-term goals?

Yes, for 5+ year goals, equity SIPs generally offer better inflation-adjusted returns than RDs due to compounding.

2. Can I lose money in SIP?

SIPs carry market risk, but volatility tends to average out over longer periods, reducing the chance of negative returns.

3. What is the minimum amount to start a SIP?

You can start with as little as ₹500–₹1,000 per month, depending on the scheme.

4. Is RD safer than SIP?

Yes, RD offers fixed, guaranteed, bank-backed returns, while SIPs offer market-linked growth with higher long-term potential.

Disclaimer:

Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. This blog is for informational purposes only and not investment advice.