Emergency Fund vs Investment in India: What Should Beginners Prioritize First in 2026?

February 27th, 2026 News

Emergency Fund vs Investment in India: What Should Beginners Prioritize First in 2026?

When starting your financial journey, one of the most confusing questions is Emergency Fund vs Investment in India — which one should come first?

Many beginners jump directly into SIPs, stocks, or crypto because they want fast returns. But without a strong financial foundation, even the best investment strategy can fail.

In 2026, with rising inflation, job uncertainty, and increasing living costs, understanding Emergency Fund vs Investment in India is more important than ever.

Let’s break it down in the simplest way possible.

Understanding Emergency Fund vs Investment in India

Before deciding what to prioritize, you must clearly understand both concepts.

An emergency fund is your financial safety net.

An investment is your wealth creation tool.

Both are important — but they serve different purposes.

The real question in Emergency Fund vs Investment in India is not which is better — but which should come first.

What is an Emergency Fund?

4

An emergency fund is money set aside specifically for unexpected financial situations such as:

-

Medical emergencies

-

Job loss

-

Sudden salary delay

-

Urgent home repairs

-

Family emergencies

Financial planners suggest keeping at least 3 to 6 months of monthly expenses in an easily accessible form.

For example:

If your monthly expenses are ₹30,000, your emergency fund should be between ₹90,000 to ₹1,80,000.

This amount should not be invested in high-risk assets.

Why Emergency Fund is Extremely Important in India

India is a fast-growing economy, but job security is not guaranteed. Private sector employees, freelancers, and business owners face income volatility.

Even during economic slowdowns, inflation continues.

The Reserve Bank of India monitors inflation and financial stability, but personal financial discipline is your responsibility.

Without an emergency fund:

-

You may take high-interest personal loans

-

You may swipe credit cards at 30–40% interest

-

You may withdraw investments during market crashes

This is why in the debate of Emergency Fund vs Investment in India, safety must come first.

What is Investment?

Investment means allocating money into assets that grow over time.

Common investment options in India include:

-

Index Funds

-

Direct Stocks

-

Real Estate

-

Gold

-

National Pension System (NPS)

The goal of investing is:

-

Beat inflation

-

Grow wealth

-

Achieve long-term financial goals

Unlike emergency funds, investments carry risk and market fluctuations.

Emergency Fund vs Investment in India: Core Difference

Let’s clearly compare them.

| Factor | Emergency Fund | Investment |

|---|---|---|

| Purpose | Financial Safety | Wealth Creation |

| Risk Level | Very Low | Moderate to High |

| Liquidity | Immediate | Depends on Asset |

| Returns | Low (3–6%) | Higher (10–15% long term) |

| Time Horizon | Short-Term | Long-Term |

This table clearly explains Emergency Fund vs Investment in India.

One protects you.

The other grows you.

Real-Life Scenario: Why Emergency Fund Comes First

4

Imagine this situation:

Rahul starts investing ₹10,000 monthly in equity mutual funds. After 8 months, the market crashes and his portfolio drops by 20%.

Suddenly, he loses his job.

Since Rahul has no emergency fund, he withdraws his investments at a loss.

Result:

-

Capital loss

-

Financial stress

-

Investment journey broken

If Rahul had built an emergency fund first, he could have survived 6 months without touching investments.

This example perfectly explains why Emergency Fund vs Investment in India is about timing, not preference.

Where Should You Keep Your Emergency Fund?

The emergency fund must be:

-

Safe

-

Liquid

-

Easily accessible

Good options include:

-

Savings Account

-

Liquid Mutual Funds

-

Short-Term Fixed Deposits

Avoid keeping emergency funds in:

-

Stocks

-

Crypto

-

Long lock-in investments

Because emergencies don’t wait for market recovery.

How Much Emergency Fund is Enough?

The ideal emergency fund depends on:

-

Job stability

-

Number of dependents

-

Health condition

-

Monthly expenses

General rule:

-

Salaried person → 3 to 6 months expenses

-

Freelancer/business owner → 6 to 12 months expenses

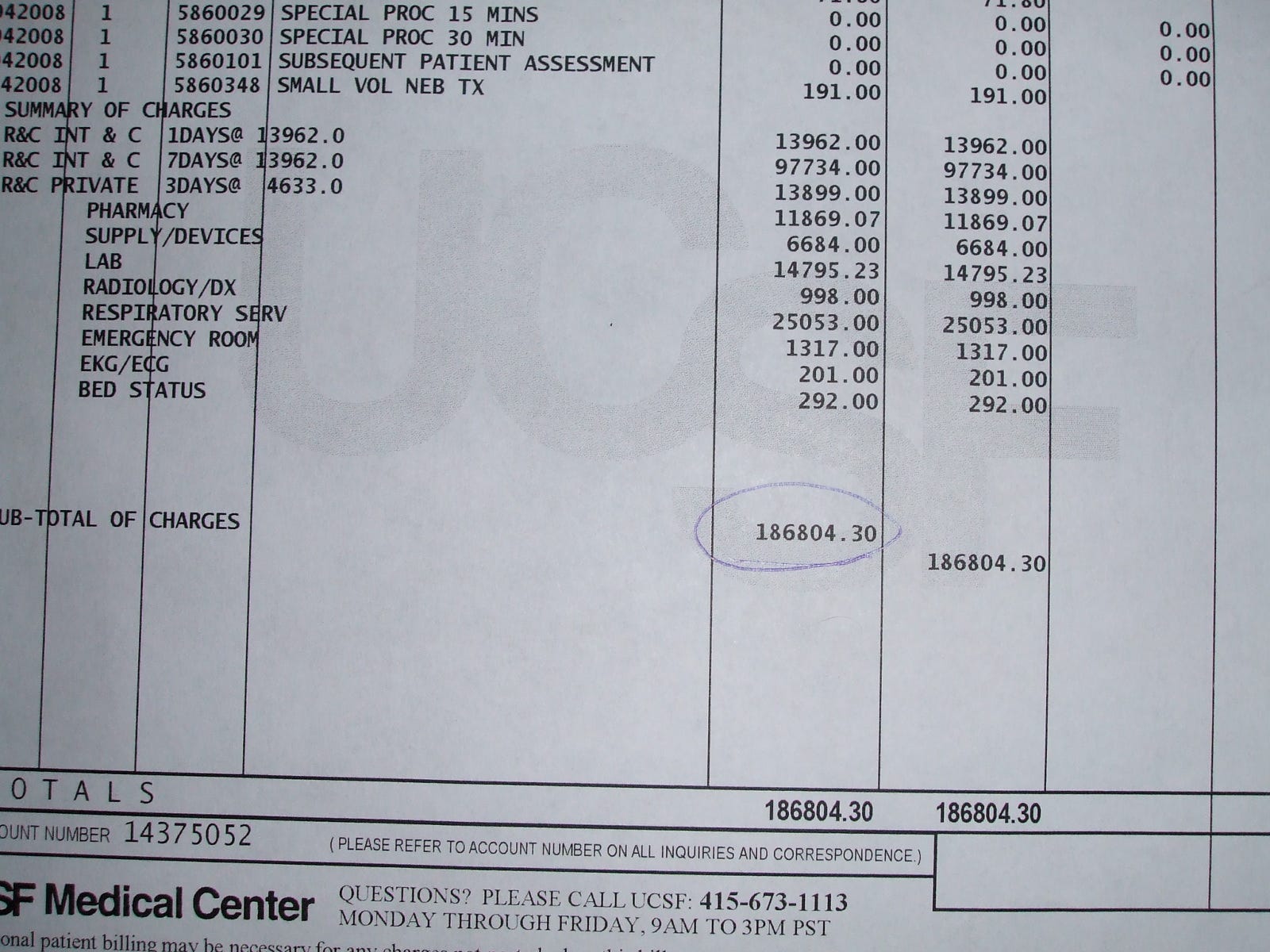

In India, medical costs are rising fast. Even a minor hospitalization can cost ₹50,000 to ₹1,00,000 in metro cities.

That is why Emergency Fund vs Investment in India must be carefully planned.

When Should Beginners Start Investing?

You can start investing when:

-

You have minimum 3 months emergency fund

-

You have no high-interest debt

-

You have stable income

-

You have financial goals

After that, start small SIP investments.

For example:

-

₹3,000 per month in index fund

-

₹2,000 per month in flexi-cap mutual fund

Gradually increase investment as income grows.

Can You Build Emergency Fund and Invest Together?

Yes — but strategically.

In 2026, a smart approach for beginners is:

-

70% savings toward emergency fund

-

30% into small SIP

This keeps momentum alive while building safety.

So in Emergency Fund vs Investment in India, the smart answer is balance — but emergency fund gets priority.

How Inflation Changes This Decision

Inflation in India averages 5–7%.

If you keep all money idle in savings, inflation reduces purchasing power.

However, without emergency protection, investments can be disrupted.

That’s why:

Phase 1 → Build safety

Phase 2 → Build growth

Phase 3 → Accelerate wealth

This structured approach wins long-term.

Psychological Benefits of Emergency Fund

Financial peace is underrated.

With emergency savings:

-

You sleep better

-

You don’t panic during market fall

-

You don’t fear job loss

-

You make rational investment decisions

Investing without safety creates emotional stress.

Understanding Emergency Fund vs Investment in India also improves financial confidence.

Common Mistakes Beginners Make

-

Investing full salary without savings

-

Taking personal loan during emergencies

-

Breaking long-term investments

-

Ignoring medical insurance

-

Overestimating income stability

Avoid these mistakes in 2026.

Step-by-Step Plan for Beginners in India

Here is a practical roadmap:

Step 1: Calculate Monthly Expenses

Rent + EMI + Groceries + Utilities + School + Insurance

Step 2: Set Emergency Fund Target

Multiply monthly expense by 6.

Step 3: Start Automatic Saving

Transfer fixed amount every month to emergency account.

Step 4: Start SIP After 3 Months Fund

Begin small investments.

Step 5: Increase Investment Annually

Increase SIP 10–20% every year.

This is the smartest approach to solve Emergency Fund vs Investment in India.

Retirement Planning Angle

If you invest aggressively without safety and face emergency withdrawal, retirement planning suffers.

Building foundation first ensures long-term compounding works uninterrupted.

Consistency beats speed.

Emergency Fund vs Investment in India: Final Verdict

Both are essential.

But order matters.

Emergency fund is the foundation.

Investment is the building.

Without foundation, the building collapses.

So in 2026, if you are a beginner in India:

✔ Build emergency fund first

✔ Then start disciplined investing

✔ Increase investment gradually

✔ Stay consistent

Conclusion

Understanding Emergency Fund vs Investment in India is the first step toward financial maturity.

Do not rush toward high returns without safety. Wealth building is a marathon, not a sprint.

Secure your base.

Then grow your wealth confidently.

Your future self will thank you.