Salary 50,000 Per Month? Here’s the Perfect Investment Strategy in India for 2026

February 28th, 2026 News

Salary 50,000 Per Month? Here’s the Perfect Investment Strategy in India for 2026

If you earn ₹50,000 per month, you are part of India’s growing middle-class workforce. But the real question is — are you using your income wisely?

In 2026, rising inflation, job uncertainty, and increasing lifestyle expenses make financial planning more important than ever. This guide explains the Salary 50,000 Per Month Investment Strategy in India in a practical and easy-to-follow manner.

Whether you are a private employee, government staff, or working professional, this strategy will help you build long-term wealth without stress.

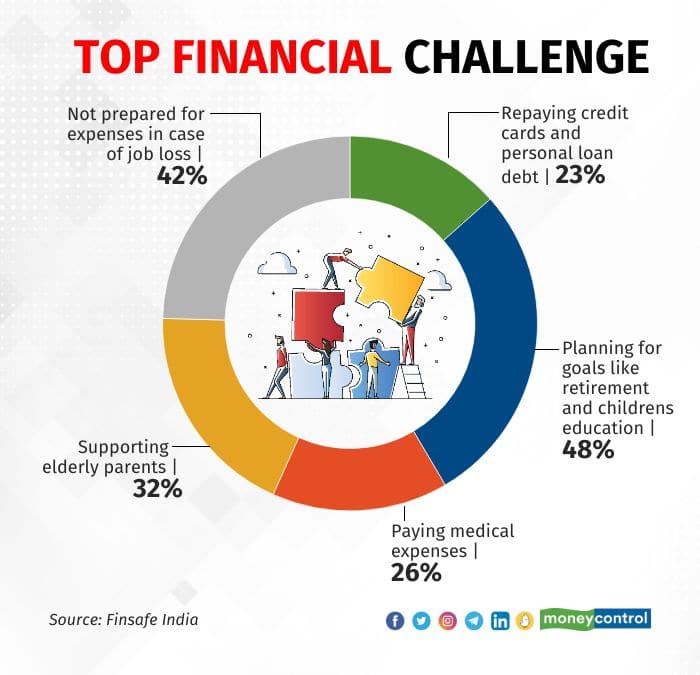

Why Proper Planning is Important in 2026

4

With inflation averaging 5–7% in India and lifestyle costs increasing in metro cities, saving money alone is not enough.

The Reserve Bank of India monitors inflation and monetary policy, but individuals must manage their own financial future.

If you earn ₹50,000 monthly and keep all money in savings accounts, your purchasing power will reduce over time.

That is why a structured Salary 50,000 Per Month Investment Strategy in India is essential.

Step 1: Understand Your Monthly Budget

Before investing, calculate your expenses.

Example breakdown:

-

Rent/EMI – ₹15,000

-

Groceries – ₹6,000

-

Utilities – ₹3,000

-

Transport – ₹4,000

-

Insurance – ₹2,000

-

Miscellaneous – ₹5,000

Total Expenses: ₹35,000

Remaining Savings: ₹15,000

This ₹15,000 is your wealth-building engine.

Step 2: Build Emergency Fund First

Before aggressive investing, build a safety cushion.

Ideal emergency fund:

3–6 months of expenses = ₹1,05,000 to ₹2,10,000

Keep this in:

-

Savings account

-

Liquid mutual fund

-

Short-term FD

This ensures you don’t break investments during emergencies.

If you haven’t read it yet, you should also check your internal blog on Emergency Fund vs Investment in India (Internal Linking Opportunity).

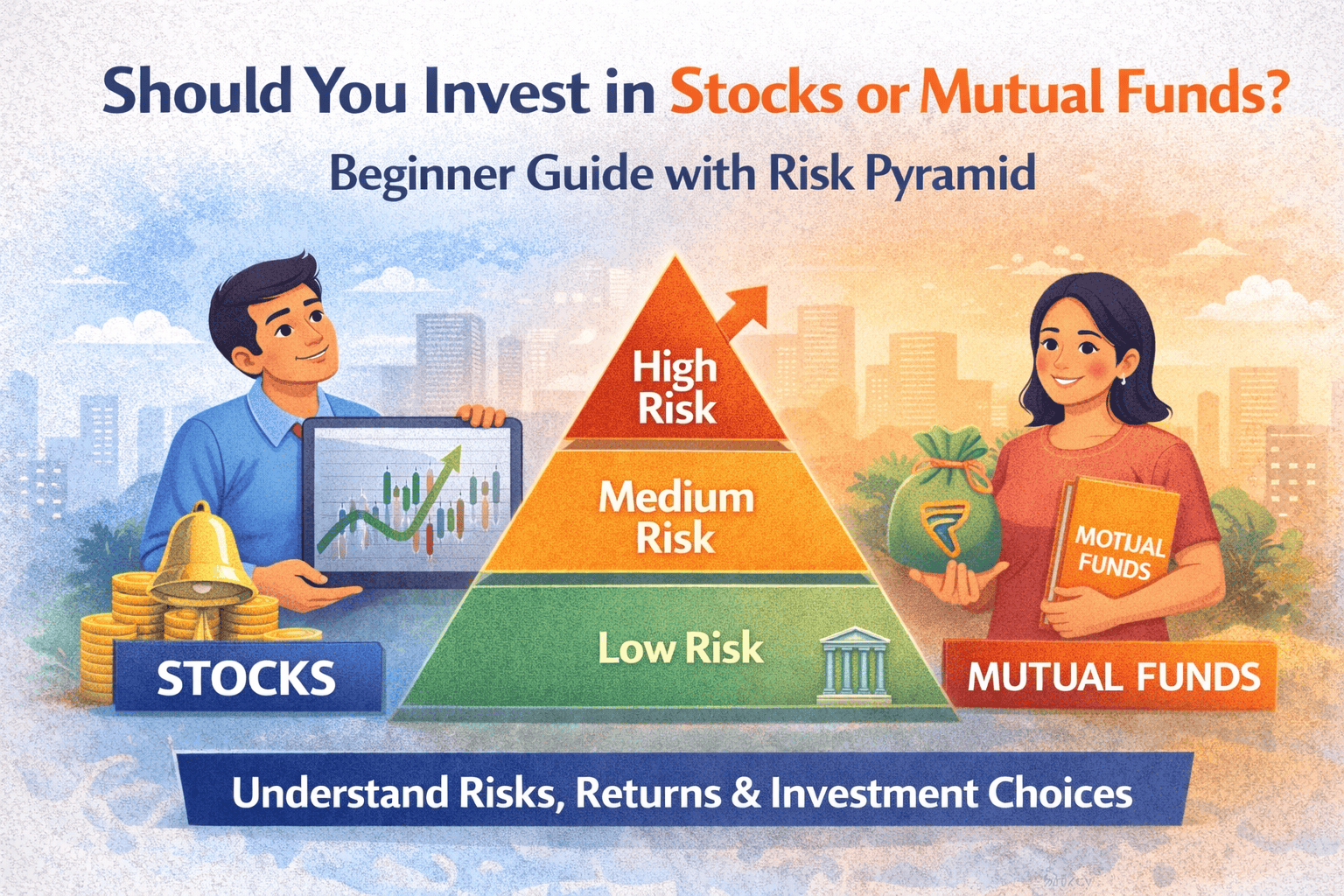

Step 3: Ideal Investment Allocation for ₹50,000 Salary

Here’s a balanced structure:

-

₹5,000 → Equity Mutual Fund SIP

-

₹3,000 → Index Fund SIP

-

₹2,000 → NPS / Retirement

-

₹2,000 → Gold ETF / Sovereign Gold Bond

-

₹3,000 → Emergency Fund (until completed)

This diversified approach reduces risk and builds growth.

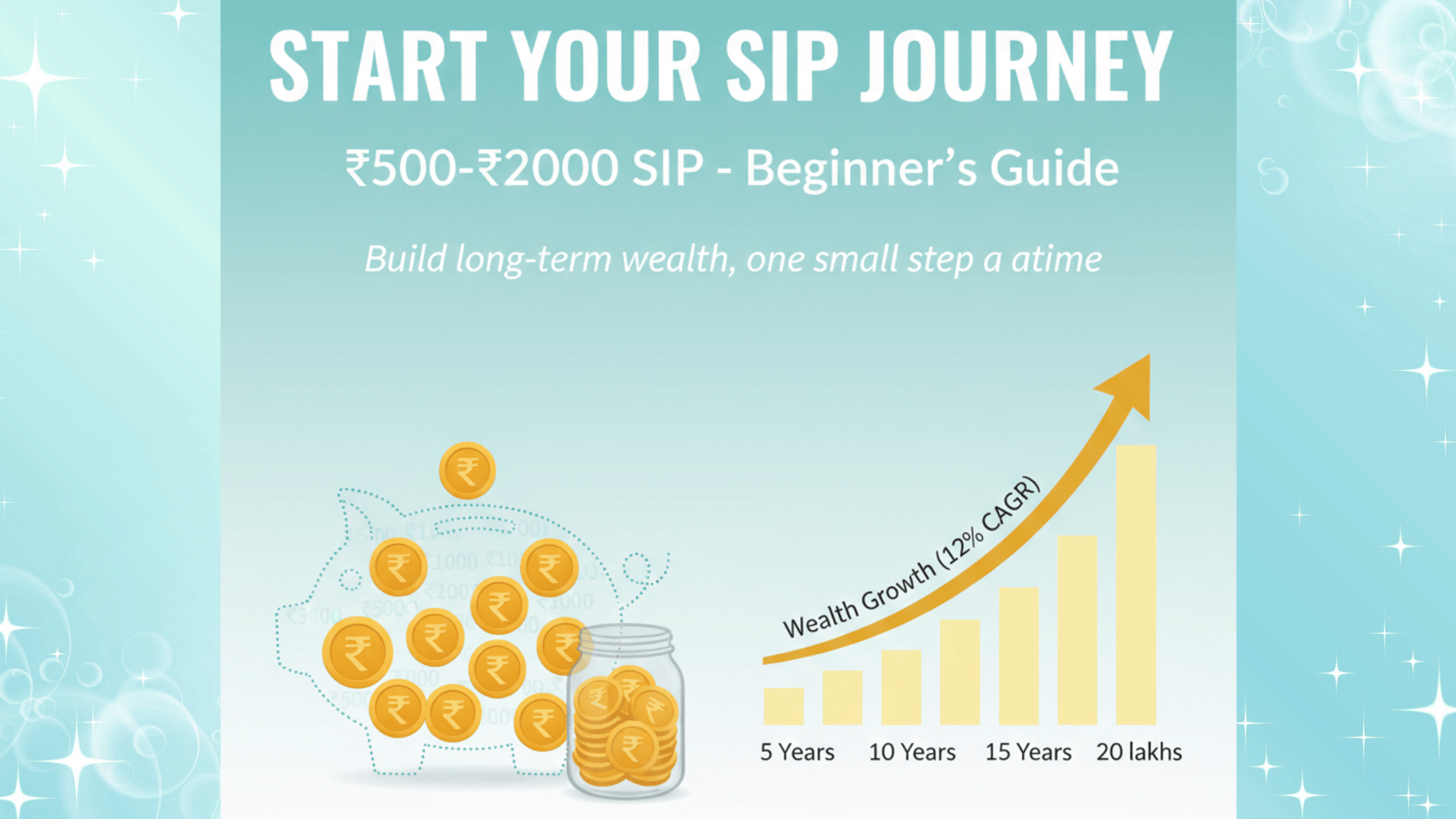

Why SIP is Best for 50,000 Salary Earners

![]()

4

Systematic Investment Plan (SIP) allows small monthly investments.

If you invest ₹8,000 monthly at 12% annual return:

-

In 10 years → approx ₹18–20 lakhs

-

In 20 years → approx ₹80+ lakhs

This is the power of compounding.

Step 4: Insurance is Non-Negotiable

Before wealth creation:

✔ Health Insurance

✔ Term Life Insurance

Without insurance, one medical emergency can destroy years of savings.

This is a key part of the Salary 50,000 Per Month Investment Strategy in India.

Step 5: Avoid Common Middle-Class Mistakes

Many salaried individuals:

-

Invest in random LIC policies

-

Keep money idle in savings

-

Take personal loans for lifestyle

-

Ignore retirement planning

Avoid these traps in 2026.

Long-Term Wealth Plan for ₹50,000 Salary

5-Year Plan

-

Emergency fund complete

-

₹8–10 lakh investment corpus

10-Year Plan

-

₹20–25 lakh portfolio

-

House down payment ready

20-Year Plan

-

₹70–80 lakh retirement fund

-

Financial stability

Consistency matters more than speed.

Can You Become Crorepati with 50,000 Salary?

Yes — but with discipline.

If you increase SIP 10% every year and stay invested for 25 years, crossing ₹1 crore is possible.

Time + Discipline + Compounding = Wealth.

Tax Planning Strategy

Use:

-

ELSS Mutual Funds (80C benefit)

-

NPS (additional ₹50,000 deduction)

-

Health insurance (80D)

This reduces tax burden and increases net investment.

You can internally link to your future blog on “Best Tax Saving Investments in India 2026.”

Salary 50,000 Per Month Investment Strategy in India – Sample Model Portfolio

| Category | Allocation | Purpose |

|---|---|---|

| Equity Mutual Funds | 40% | Growth |

| Index Funds | 20% | Stability |

| NPS | 15% | Retirement |

| Gold | 10% | Hedge |

| Emergency Fund | 15% | Safety |

This balanced strategy works for most salaried individuals.

Psychological Discipline for Wealth Creation

Investing is not only financial — it’s emotional.

Markets will fall.

Expenses will rise.

Friends will show luxury lifestyles.

Stay consistent.

Long-term investors win.

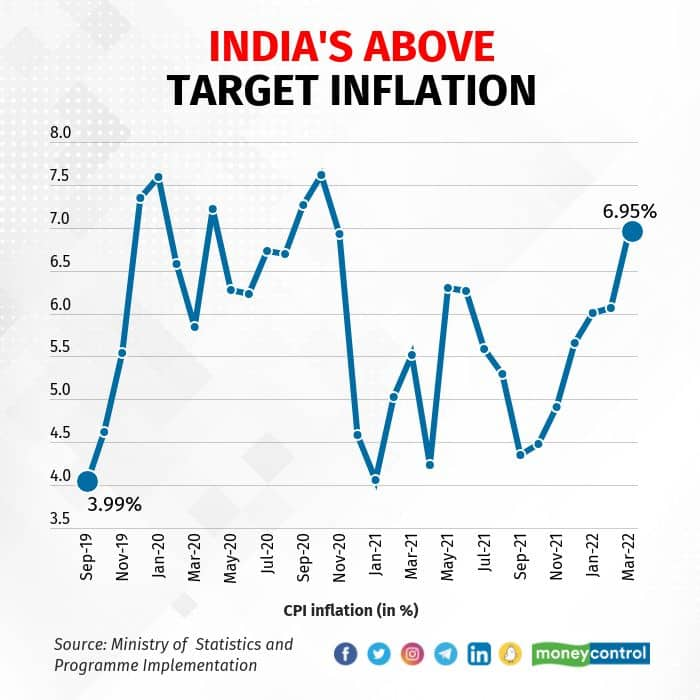

Inflation Impact on 50,000 Salary Earners

4

If expenses grow 6% annually:

₹35,000 expense today → ₹63,000 in 10 years.

Without investing, savings won’t survive.

This proves why the Salary 50,000 Per Month Investment Strategy in India must focus on growth assets.

Final Conclusion

If you earn ₹50,000 per month, you are not late.

You just need structure.

The perfect Salary 50,000 Per Month Investment Strategy in India includes:

✔ Budget discipline

✔ Emergency fund

✔ SIP investments

✔ Insurance protection

✔ Long-term mindset

Start today. Increase gradually. Stay consistent.

Wealth is built slowly — but surely.